ITR Filing Due Dates for FY 2025-26 (AY 2026-27)

The Income Tax Department has prescribed different due dates based on the type of taxpayer and the applicable ITR form. Filing your Income Tax Return within the due date helps avoid penalties, interest, and compliance issues. For Assessment Year (AY) 2026-27, the due dates are as follows:

| ITR Form | Taxpayer Category | Due Date |

|---|---|---|

| ITR-1 (Sahaj) | Salaried Individuals, Pensioners, Resident Individuals (Non-Audit Cases) | 31 July 2026 |

| ITR-2 | Individuals & HUFs without Business Income | 31 July 2026 |

| ITR-3 | Business Owners & Professionals (Non-Audit Cases) | 31 August 2026 |

| ITR-4 (Sugam) | Presumptive Taxation Scheme Assessees (Non-Audit Cases) | 31 August 2026 |

| ITR-5 | LLPs, Partnership Firms, AOPs, BOIs (Audit Cases) | 31 October 2026 |

| ITR-6 | Companies | 31 October 2026 |

| Transfer Pricing Cases | Taxpayers covered under Section 92E | 30 November 2026 |

ITR 1 to ITR 6: Complete Guide to Income Tax Return Forms in India (FY 2025-26)

Introduction

Filing an Income Tax Return (ITR) is a mandatory compliance requirement for eligible taxpayers in India. The Income Tax Department has introduced different ITR forms to cater to various categories of taxpayers based on their income sources, residential status, and business structure. Choosing the correct ITR form is crucial because filing an incorrect return can lead to notices, delays in processing, or rejection of the return.

In this comprehensive guide, we will discuss ITR-1, ITR-2, ITR-3, ITR-4, ITR-5, and ITR-6, their applicability, eligibility criteria, income sources covered, and key differences among them.

What is an Income Tax Return (ITR)?

An Income Tax Return (ITR) is a form through which taxpayers declare their income, deductions, tax liability, and taxes paid during a financial year. Filing an ITR helps maintain tax compliance and serves as proof of income for loans, visas, tenders, and other financial transactions.

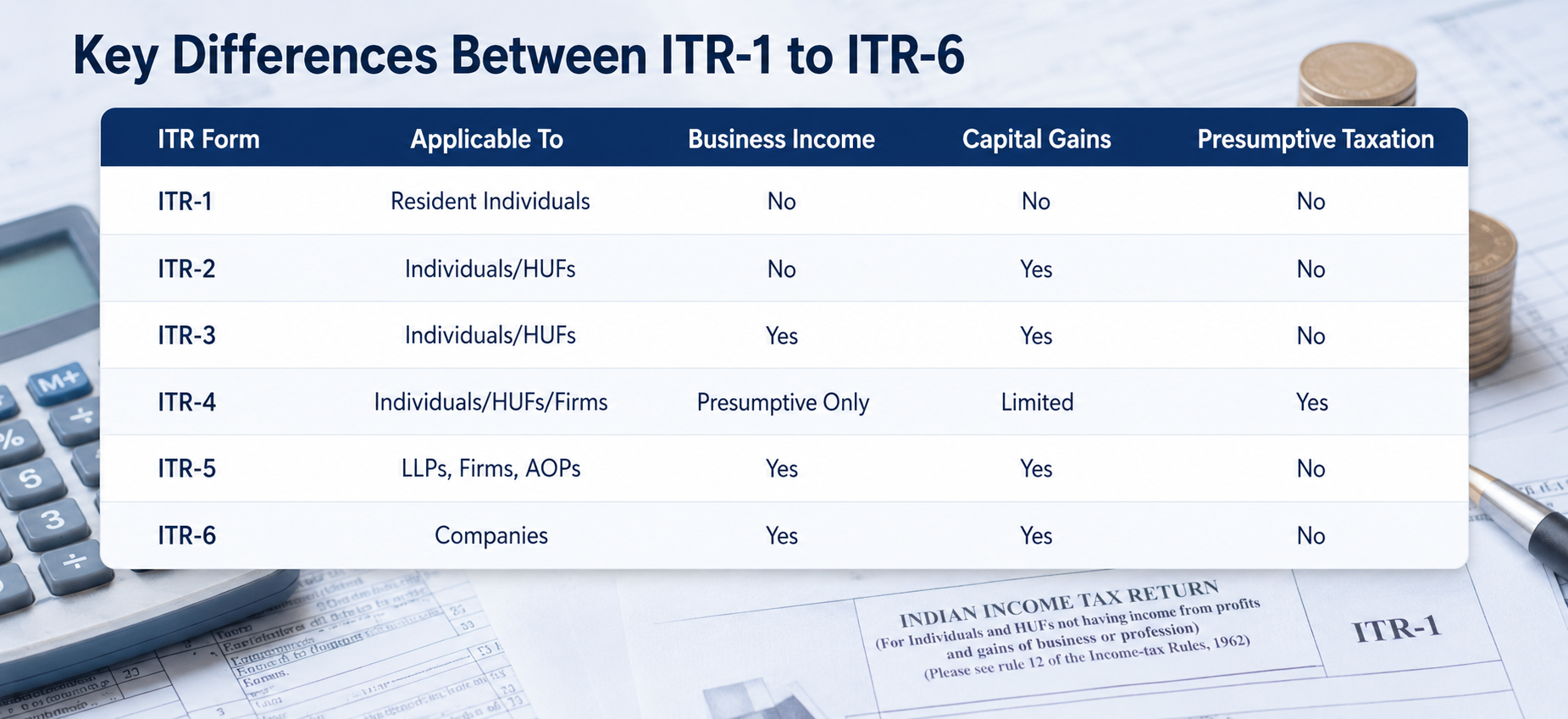

ITR-1 (Sahaj)

Who Can File ITR-1?

ITR-1, also known as Sahaj, is the simplest income tax return form meant for resident individuals having:

- Total income up to ₹50 lakh

- Income from salary or pension

- Income from one house property

- Income from other sources (excluding lottery and racehorses)

- Agricultural income up to ₹5,000

Who Cannot File ITR-1?

An individual cannot file ITR-1 if:

- Total income exceeds ₹50 lakh

- Has capital gains income

- Owns foreign assets

- Has foreign income

- Is a director in a company

- Holds unlisted equity shares

- Has business or professional income

Benefits of ITR-1

- Simplified filing process

- Minimal disclosure requirements

- Faster return processing

Example

A salaried employee earning ₹12 lakh annually with bank interest income can file ITR-1.

ITR-2

Who Can File ITR-2?

ITR-2 is applicable to individuals and Hindu Undivided Families (HUFs) who do not have business or professional income.

It can be filed by taxpayers having:

- Salary or pension income

- Income from multiple house properties

- Capital gains from shares, mutual funds, or property

- Foreign assets and foreign income

- Agricultural income exceeding ₹5,000

- Income exceeding ₹50 lakh

Who Cannot File ITR-2?

- Individuals having income from business or profession.

Key Features of ITR-2

Capital Gains Reporting

Taxpayers must report:

- Short-term capital gains

- Long-term capital gains

- Sale of listed shares

- Sale of mutual funds

- Sale of property

Foreign Asset Disclosure

Residents holding foreign assets must disclose:

- Foreign bank accounts

- Foreign investments

- Foreign properties

Example

A salaried employee who sold mutual funds during the year and earned capital gains must file ITR-2.

ITR-3

Who Can File ITR-3?

ITR-3 is meant for individuals and HUFs having income from:

- Business

- Profession

- Proprietorship firms

This form is commonly used by:

- Chartered Accountants

- Doctors

- Lawyers

- Architects

- Consultants

- Freelancers

- Traders

Income Covered Under ITR-3

Business Income

- Retail business

- Manufacturing business

- Trading business

- Commission income

Professional Income

- Consultancy services

- Legal services

- Medical practice

- Technical services

Other Income Sources

In addition to business income, taxpayers can report:

- Salary income

- House property income

- Capital gains

- Interest income

Important Information Required

- Balance Sheet

- Profit & Loss Account

- GST details

- Tax Audit details (if applicable)

- Depreciation schedules

Example

A freelance digital marketing consultant earning ₹18 lakh annually must file ITR-3.

ITR-4 (Sugam)

Who Can File ITR-4?

ITR-4, also called Sugam, is designed for taxpayers opting for the presumptive taxation scheme under:

- Section 44AD

- Section 44ADA

- Section 44AE

Applicable taxpayers include:

- Resident individuals

- HUFs

- Partnership firms (excluding LLPs)

with total income up to ₹50 lakh.

Presumptive Taxation Scheme

Under presumptive taxation:

- Books of accounts are not mandatory.

- Income is presumed at a fixed percentage of turnover.

Section 44AD

Applicable to small businesses.

- 8% of turnover deemed as income.

- 6% for digital receipts.

Section 44ADA

Applicable to professionals.

- 50% of gross receipts deemed as income.

Section 44AE

Applicable to goods carriage operators.

Who Cannot File ITR-4?

- Companies

- LLPs

- Non-residents

- Taxpayers with income exceeding ₹50 lakh

- Taxpayers having foreign assets

Benefits of ITR-4

- Simplified compliance

- Reduced documentation

- No detailed books of accounts required

Example

A freelance graphic designer earning ₹25 lakh and opting for Section 44ADA can file ITR-4.

ITR-5

Who Can File ITR-5?

ITR-5 is applicable to entities other than individuals and companies.

Eligible entities include:

- Partnership Firms

- LLPs

- Association of Persons (AOPs)

- Body of Individuals (BOIs)

- Artificial Juridical Persons

- Cooperative Societies

- Business Trusts

- Investment Funds

Key Features

Comprehensive Reporting

ITR-5 requires:

- Balance Sheet

- Profit & Loss Account

- Capital Accounts

- Partner Details

- GST Information

LLP Compliance

Limited Liability Partnerships (LLPs) are specifically required to file ITR-5.

Example

An LLP engaged in software development must file ITR-5.

ITR-6

Who Can File ITR-6?

ITR-6 is meant for companies registered under the Companies Act, except those claiming exemption under Section 11.

Applicable To

- Private Limited Companies

- Public Limited Companies

- One Person Companies (OPCs)

- Foreign Companies operating in India

Key Information Required

Financial Statements

- Audited Balance Sheet

- Profit & Loss Account

- Auditor’s Report

Tax Computation

- MAT (Minimum Alternate Tax)

- Depreciation

- Brought Forward Losses

- Deductions and Exemptions

Corporate Disclosures

- Shareholding details

- Director details

- Related party transactions

Filing Requirement

ITR-6 is required to be filed electronically using a Digital Signature Certificate (DSC).

Example

A Private Limited Company engaged in manufacturing operations must file ITR-6.

Common Mistakes While Filing ITR

Choosing the Wrong ITR Form

Many taxpayers select the wrong form, leading to defective return notices.

Incorrect AIS Reconciliation

Always reconcile:

- Form 26AS

- AIS (Annual Information Statement)

- TIS (Taxpayer Information Summary)

before filing.

Non-Disclosure of Capital Gains

Failure to report share or mutual fund transactions can result in tax notices.

Incorrect Bank Details

Wrong bank account details may delay refunds.

Ignoring Foreign Asset Disclosure

Foreign assets must be reported wherever applicable.

Benefits of Filing ITR on Time

- Avoid late filing fees

- Faster tax refunds

- Easy loan approvals

- Visa application support

- Carry forward of business and capital losses

- Better financial credibility

Conclusion

Selecting the correct Income Tax Return form is one of the most important steps in tax compliance. ITR-1 is suitable for salaried individuals with simple income, while ITR-2 caters to taxpayers having capital gains and foreign assets. ITR-3 is used by professionals and business owners, whereas ITR-4 simplifies compliance under the presumptive taxation scheme. ITR-5 is applicable to LLPs and partnership firms, while ITR-6 is mandatory for companies.

Understanding the applicability of each form helps taxpayers avoid errors, ensure timely compliance, and maximize available tax benefits. Before filing your return, review your income sources carefully and choose the appropriate ITR form to ensure smooth processing by the Income Tax Department.

Keywords: ITR Forms, ITR-1, ITR-2, ITR-3, ITR-4, ITR-5, ITR-6, Income Tax Return Filing, Types of ITR Forms, Income Tax Return India, ITR Filing FY 2025-26, Tax Return Forms, Presumptive Taxation Scheme, Income Tax Compliance, Tax Consultant Services.